In this episode of Fintechfun, Chris Titley chats with Anson Parker, the Chief Product Officer at Upbank, about his journey in the fintech industry and the evolution of Upbank as a leading digital banking platform. From the early days of conceptualizing a new kind of banking experience to the current focus on innovative features like “pull to save” and the upcoming subscription offering “Up High,” Anson shares insights on how Upbank is redefining the future of banking. Key themes discussed • Anson’s background in software development and the founding of Upbank. • The importance of user feedback and balancing creativity in product development. • The introduction of unique features like “pull to save” and “Maybuy” to enhance the banking experience. • The upcoming subscription offering “Up High” and its potential to revolutionize banking fees and customer benefits.

Anson’s journey from software development to reimagining the banking industry with Upbank.

The focus on user-centric product development and the balance between innovation and customer feedback.

The impact of features like “pull to save” and “Maybuy” in creating engaging and personalized banking experiences.

The introduction of the subscription offering “Up High” as a new way to provide additional value and benefits to customers.

The importance of transparency, collaboration, and customer engagement in shaping the future of banking.

Upbank Website

Transcript Synced · click any line to jump ▾

Chris Titley: You're listening to a Day One FM show.

Anson Parker: Pick My Brain is the podcast where founders pitch me their startup and I try to give them some useful advice so they can connect better with potential co-founders, investors, media, and of course, customers. My name's Alan Jones and I was a founder myself for about 15 years, and after that, an angel investor for another 15 years. So yeah, old. Some of my ventures have been successful and some failed disastrously, But I like to think I've learned a thing or two along the way, and maybe some of that can help you. So if you'd like to learn how to tweak your pitch, subscribe to the Pick My Brain show now, wherever you like to listen to podcasts.

Chris Titley: If you're building a SaaS business, achieving compliance with SOC 2, ISO 27001, or other in-demand frameworks can unlock major growth for your company and establish customer trust. However, this process is often time-intensive and very costly. Vanta automates up to 90% compliance, getting you audit-ready quickly and saving up to 85% of associated costs. And Vanta scales with your business with a market-leading trust management platform to help you continually monitor compliance, unify risk management, and streamline security reviews. Join 7,000 global companies like Atlassian and Dovetail that use Vanta to build trust and prove security in real time. My listeners get 10% off Vanta when they go to vanta.com/fun. That's vanta.com/fun. Hi, I'm Chris Tittley, and this is FinTech Fun, the podcast where I speak with Australian fintech founders and executive management and have some fun along the way, gaining insights about the person behind the brand. FinTech Fun is part of Day One, the network dedicated to founders, operators and investors. I'm joined by Anson Parker, Chief Product Officer at UpBank. Anson, thanks so much for being part of this series.

Speaker C: Pleasure, Chris. Thanks for having me on.

Chris Titley: Now, a lot of listeners out there will know the Up brand, but they might not know a little bit about you and how important you are to the organisation. Let's go back a little bit on when you joined Up and a little bit about background about yourself and why you joined.

Speaker C: Yeah, it depends how far you want to go back, but, you know, I started off, I guess, in the software business building websites and that sort of took me, you know, to Sydney and over to the US for a couple of years where I met my now wife. My startup didn't do so good. We kind of ran out of money and she was very interested in moving to Melbourne. She has an arts background and so she sort of dragged me down here. And it wasn't long before I got introduced to a couple of interesting blokes, Dom Pym and his co-founder Grant Thomas. And they were looking to kind of innovate and do something different in the banking space.

Anson Parker: Mm-hmm.

Speaker C: Which is not an industry I ever thought I would work in. At the time in Melbourne, that was, a lot of jobs were in banking and I was like, yeah, never applying for those. But you know, the opportunity to kind of get in there and bring in a lot of the sort of modern software ideas, not just be working in a big 200-person kind of developer shop using enterprise tools and all that kind of stuff, you know, which I think a lot of people were doing. If you're in that space at the time, it was kind of the cost of admission.

Chris Titley: Mm-hmm.

Speaker C: But to really go in with sort of modern thinking and kind of set a vision was a really interesting challenge because as a customer of banking, I was always kind of frustrated at how crappy I thought it was and how much potential I thought there was for it to be better. But that first incarnation, really, we were a bit of a services style model. We actually didn't have, we hadn't created Up yet, so we were kind of really solving problems for a bank, Bendigo Bank, that was based down here in Victoria and kind of reimagining banking for their customer base. And sort of trying to put a lot of these ideas into action. And it was probably not for about 4 years until we really got the, probably got the itch to say, what if we could really just go out and do this ourselves and have full control and, you know, own the brand and really own the sort of experience from, you know, the whole way through and put a lot of the ideas that maybe we hadn't quite been able to get over the line, you know, in a more sort of services vendor relationship, yeah, into practice as a more of a a product company. And that was in some ways the start of Up.

Chris Titley: I'm interested to know, working for Bendigo, and there's always been a strong relationship between Ferrocia and Bendigo, and obviously Up is now owned by Bendigo. But at the time when you were working for Bendigo and you had these ideas, and then eventually you're like, oh, it'll be under the Bendigo banner and these ideas will come through onto Bendigo's customers, then that sort of split of going, actually, there's something here to build a a niche brand or a different brand. How did that sort of conversation start and how did the sort of the name of Up and, you know, that begin?

Speaker C: Yeah, we learned some lessons, I think, working in that services model and basically building software for an existing customer base. You know, that's, that's a really challenging thing to do, as it turns out. And I think the interesting thing about banks is they have this complete saturation of the market. Effectively, every adult Australian has a bank account. And, you know, these big brands have this incredibly broad customer base, both in terms of like life stages, but also just kind of financial configurations. And there are businesses on there and clubs, and there's just so, so much variation, so many different ways people access this stuff. You realize that, you know, that's a heck of a challenge to actually do anything that everybody's gonna like in that space because you have such a broad church, so to speak. And I think that we saw all these amazing innovations and capabilities that were coming online, and you have to be able to, you know, you can't rely on those to get to such a broad customer base. So the idea of sort of focusing in on a specific kind of, you know, niche, I guess you would call it, and, you know, Up is very, you know, started as very much just a transactional account savings and really resonated with the young customer base that obviously all had smartphones to join. You know, when you sort of focus down to that, then you can really take advantage of all of the new capabilities and innovations coming online because you're not trying to sort of like, bring along this, this huge range of people and platforms with you. And I think that was one of the most intriguing parts of the opportunity was to really get to explore that space.

Chris Titley: And then under the brand UP and then when the launch happened and sort of the beta launch and the beta testing and then growing from, from zero customers, broadly speaking, to where you are now, I think the last Bendigo figures are somewhere north of 800,000 or around 800,000. Customers, why do you think people morph towards Up and what are they doing differently? And going back to some of the early features that I suppose was the hook for some people to go, actually, this is really fun, before we get onto the challenges of the new products, et cetera. But what was the initial kind of hook to get people going, hey, this is reimagining banking?

Speaker C: Yeah, I think it's actually one of the more difficult parts of the journey has been that because As software people, you think, "We'll build something great and people will just naturally want it." But of course, you have this friction, particularly with money and people's banks, where that high perceived cost of switching, like we talk about a lot in the industry, which is even if maybe it's not so much work for people to move to a new bank, in their minds, it is actually a lot. And so it's not enough to be just that bit better than the competition. I think you really have to come to market with something really different. And that was great for us because we were really interested in kind of reimagining the space and bringing this kind of software first principles approach to the space, which I don't think we'd really seen yet. And so everything from just basically throwing out all of those assumptions. And I think that a lot of the early digital banking, online banking, it's kind of that early stage you see with a lot of technology where the first cut is really taking the real world sort of forms and digitizing them, right? Payments in an app or on a website was this idea— it's effectively the form you'd take off the carousel in branch and fill out. And there's a few things that software has done to make that a bit faster to fill out, but it hadn't fundamentally changed that idea. It was paying money into another bank account. And, you know, on the upside, we're like, this isn't paying money into another bank account. I mean, of course it is, but it's really an exchange between two people. And that exchange is more like a conversation, or could be more like a conversation if we— if that's how we framed it. So I think there was kind of those big ideas, but there's also, I think, just a different approach, which was like, for us, the experience itself was the product. It's not the sort of financial instruments beneath that. And I feel like banking for a long time has had a mindset of, you know, what are your products and what are the channels you distribute those products on? And so it's a very— You know, I think when you say, no, the experience is the product, it's not about the financial products, about what those do for people and how they relate to them. And the engagement of that experience, I think, is what has set Up Apart apart. And that has led to, I think, ultimately the growth, because when people become, you know, engaged and huge advocates, then that word of mouth really is enabled by that. And that's really, you know, 80% of our growth. And, you know, 80% of that growth to 1 million customers later this year is really driven by that, by that advocacy, that genuine advocacy and word of mouth.

Chris Titley: Absolutely. And in regards to the products, which is your area, some of the early products that I remember were sort of swipe up to save a cent or round up, et cetera. But then also some of the challenges I remember from the early days where you didn't have the BPAY functionality or you didn't have joint accounts, which ended up becoming 2UP and sort of joint accounts reimagined. That sort of feedback from customers early on versus your innovative mindset going, we're releasing this product, and then I was going, hold on, so you don't even have BPAY? How did you manage that? Um, and I suppose, how do you, how do you, how do you prioritize the products from A, user feedback, and/or B, your creativity?

Speaker C: You know, Up was very much that, you know, that lean startup mindset of like, get that minimum viable product into market and go from there. And for us, that meant launching, uh, without payments of any kind. So really, you could download an app, you could add money to it. The only way to use that money was to tap a card at a, at a merchant or, or grab cash out of an ATM. So very, very minimum. And, you know, I think again that meant we could get into market and start to validate some other things early. I mean, that's the point of doing it. But as you say, like, especially in a very mature space when the expectation of that what table stakes functionality is, is very high, right? We can't just gradually discover those things as as well as a new industry mature, like say maybe social media or something else has done. So for us, that meant how do we, you know, how do we reassure people, right, that, okay, today this is doing a few things, hopefully really well and differently, but over time it'll expand out. And one of the ways we did that was by being transparent about that and publishing, you know, our roadmap, which we called it like the Tree of Up, which was a very sort of visual, engaging way to understand that Okay, these guys are going to become a bank at some point and provide all that functionality that I would expect, and this is kind of the way they're doing it. And I think, you know, we also just really focused on releasing fast, releasing often, and so building that trust and confidence in people's minds that we're actually going to get there relatively quickly, even if we didn't have it today.

Chris Titley: Mm.

Speaker C: I think like in terms of like, you know, do we build BPAY or do we build some— something that may seem a bit gimmicky, right, like a pull-to-save, I mean, I feel like we've, you know, like the brilliant thing about the Up journey is the trust we've had from the original founders and from Bendigo now to make these bets and to try new things and kind of do things our own way. And for us, like a feature like, you know, pull to save, which, you know, for listeners, I guess, that don't know what I'm talking about, effectively that pull to refresh gesture that you'd use on email, in Up, if you do that, it'll flick the spare change of your balance into a savings account. I think that feature is amazing for a couple of reasons, I guess if I do say so myself. The first is that it signaled— the reason we're able to build it was because we got rid of pull-to-refresh. We actually introduced this completely real-time nature of apps so that if you had the app open and your credit card or your debit card, I should say, got charged, you would see that transaction happen, or if someone paid you, you would see that. You didn't ever need to refresh anymore, it was just always kept up to date. And so that was an amazing, I think, step forward for us to then be able to just conceive of banking as a real-time medium, not as something you sort of log in and you see stuff and then you log out. But also just as a great way for people to— UP has so many features and moving parts, it can probably be quite a hard thing to explain to someone, right? Like, why is this good? Why should I consider this?

Anson Parker: Mm-hmm.

Speaker C: So having really interesting, like, fun ways to demo how UP is different. Like pulling a coin down from the top of the screen and flicking into a savings account. I think those things say a lot about Up's approach and Up's mindset. And I think they're just great ways actually for us to sort of give people tools to spread the word.

Chris Titley: You mentioned the word bet then in terms of like a product which people might use or might not use. Some bets may not work and some bets, obviously like the pull up to save works. What's something that you're most proud of proud of it on up and seeing the progress from a product point of view of where that, you know, where that has gone? Obviously that Flick to Save one has generated millions of dollars of savings for people, but is there others there that you're proud of as well?

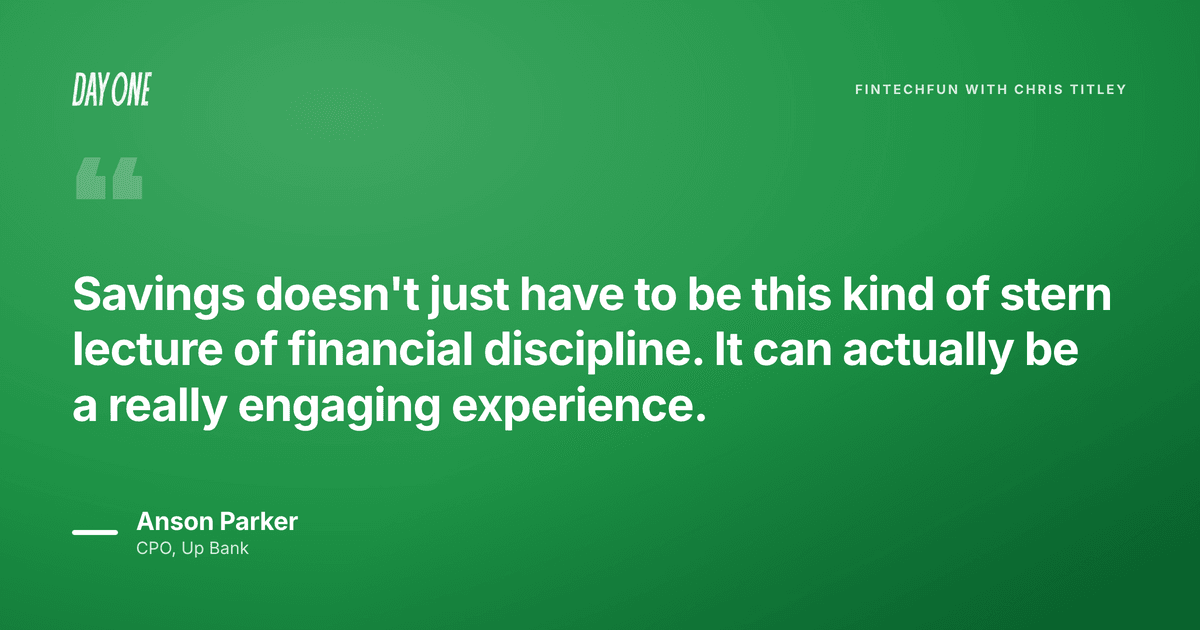

Speaker C: I mean, I really love a feature we built called May Buy, which was kind of a twist on the buy now, pay later space, which, you know, at the time we launched that feature, I mean, I think that space is still enormous, but just with all the press that and media attention was getting at the time too. I mean, every, it seemed like every, every bank in the country was going from sort of critics of the space to then jumping on board and launching their own product. And we really liked this idea that we could sort of reimagine, take the sort of really like engaging, almost like take the dopamine hits out of instant gratification that these offerings really kind of, I guess, you know, play in and, but flip that around for savings. So we built this idea that you would, find a product online, like browsing on your mobile phone, and send that product to your banking app, which is pretty wild. Um, and then we would pull that in and give you just like a 4-part, uh, installment plan to save for that, right? So instead of buying it on the spot, you're building savings for it in that same sort of Save Then For style model. And obviously that you don't get the product day one, but, but we saw that as a feature. You kind of get the dopamine hit of like, I've got this thing, I'm working towards it, But if I decide at any point along that journey, you know what, I don't really want this anymore, or once I've saved up for it and that the cost of that item is maybe a bit more real, you know, that I could decide I actually, I'd rather just have that money and use it for something else. So I think that it just is a great, it's a great sort of, I think, demonstration where you can sort of play in, play in the like fun, you know, engaging space. Like savings doesn't just have to be this kind of stern lecture of like financial discipline, right? Yeah. It can actually be like a really engaging experience and that, And, and that experience can teach you lessons without being patronizing or kind of, you know, paternalistic or whatever the word is.

Chris Titley: Yeah, no, I agree. And that's something which, as a parent, it's a bit of a tricky one to sort of educate your kids around savings. And because generally when they save $3, they want to go and buy a Slurpee or something. So anyway, uh, interesting. Well, moving on to the future of, of banking, and there's probably some things that, that are in the pipeline for Up, and some things you might want not be able to tell me, but some things you might be able to tell me. What, when you have a chat at Up and say, well, what's next and what can we do, what's something which sort of springs to mind around the future?

Speaker C: Well, I think a really, um, like a really interesting one is, um, this idea of, uh, of a subscription offering in Up, um, which we're calling Up High. So that's Like, I guess the one-line sort of pitch for that is, can we make something compelling enough that customers choose to pay for it? And it's effectively flipping the idea of bank fees on its head, right? Like, Up is sort of no monthly fees. We're very much a fee-free operation. So we're not imposing fees for using Up. But what if customers actually wanted to pay us a fee for additional value and benefits? And I think this could be seen as like, hey, is this a way for banks to reinvent what bank fees are that's putting the customer at the center? But for us, I mean, it's really just, hey, can we go off and really get weird with features or, you know, build in these additional benefits that people really want? It's sort of a license, I think, in a way for us to really, you know, I guess as a business scales and matures and you get these, you know, your business strategies and your revenue targets, you know, I think it is, it's always a challenge to like keep making those bets, keep exploring things. And in some ways I love UpHigh as an opportunity to make that exploration and fun, like almost like a commercial enterprise, you could say, right? I think we can always do an element of it without, without it, but I think it just enabled us to kind of double down in that space. Mm-hmm. So I think that one's, you know, interesting. And, you know, the sorts of things we do, I think will be, will be really interesting over time. We're at, we're very early days. So we've basically just kind of, we did a bit of a temperature check to see if people would even want this. And I think that was really important to us, and we got really overwhelmingly positive response to that. So we've kind of gone to the next stage, which is this very much an early access program where we're like, instead of us going away for 2 years and building stuff and coming back and saying, hey, we've got a subscription offering, let's have people join a program for a little one-off fee to just kind of get what we've got today and build it with us so we can release new stuff. And we're not going to start charging monthly subscriptions for that until people are like, yep, this is totally worth it. Mm-hmm. And so I think that's just like a very different model for banks, for a bank to basically engage with customers and develop value in collaboration with customers. So, you know, I'm fascinated to see where that goes. And, you know, I think the great thing is it's a bet, you know, like maybe it won't work. Maybe we'll not find that, that point where people like, you know, I'll pay for this. Like, we don't really know where it's going to go.

Chris Titley: Is it sort of a bit like economy versus business class? But with business class, you also get the you also get the testing. Yeah.

Speaker C: Well, I mean, I think that's my issue with that analogy is probably like my theory on business class, at least my hot take, is like business class is only good because economy sucks, you know? Like, it's not like this class is actually good. Like, the food in business class is probably like pretty average food. If you went to like a restaurant and got that, you're like, ah, yes, that was okay, right? Like, so we don't want to be in a model where we're like, oh, the free products kind of a bit crap or like pretty limited and which, you know, it's a common sort of freemium like model, right? Where it's like, oh, you can do a little bit in free and then as soon as you want to do more, we'll charge you. We'll sort of put these ceilings in that you're going to hit. That we really try and avoid. We're really trying to avoid that with the paid product. Of course, everyone wants everything for free, but if we want to maintain that really, really strong free product, that's going to work for most people out of the box. And the sort of things you might pay for might be more about, hey, I want more configurability or additional stuff that maybe I don't need. Not just kind of like, hey, my meal sucks in economy. Yeah, okay. And if I want a half-decent bite, I gotta pay.

Chris Titley: Well, there you go. Well, that certainly explained that analogy and why that analogy is not so with UpHigh. So I thought there might've been a reference with the high being in the sky and aeroplanes, et cetera, but maybe not. Anson, thank you for talking about the, I suppose, early up days to where you are now and all the products. And obviously being the Chief Product Officer, you're pretty well known, but also not as well known as some of the founders, I suppose. Can you talk about yourself? And what you do in your downtime. And is there something out there that some of the listeners might not know a little bit about you?

Speaker C: Yeah, sure. I mean, I'm a, well, originally a Kiwi, but live in Melbourne now. I have a young family. We have, I have 3 kids somehow. So we have a 7-year-old boy and we had twin girls 3 years ago. So we're fabulously busy running around after them. You got that. So when I'm not at work or running after them, I'm, I do a bit of home brewing. I'm pretty— Oh, right. Pretty passionate about that. And like to cook things over fire and then probably run those calories off every now and then with a bit of jogging. And I'm learning to surf as well, which is humbling in, you know, in your 40s. That's a— it's a tough time to take up a sport like that, but I think, you know, it's pretty fun as well.

Chris Titley: So two questions on the back of that. One, what's your favorite beer then, if you're a brewer? And secondly, your TV shows of choice for your kids. Do you get into Bluey?

Speaker C: Bluey's amazing, and, uh, I— my claim to fame on Bluey is the, the guy who does, uh, is it Bingo the dad?

Chris Titley: Is that the— uh, no, no, no, it's Bluey and Bingo. It's, um, Bandit, isn't it?

Speaker C: Bandit, yeah, sorry. Uh, I think it's Dave McCormack. Yes, who does the dad's voice. He was in a band called Custard, Brisbane-based. And one time I went into a CD store in, I think, the very late '90s and bought a Custard CD, and the person in the shop was like, hey, that guy's like the lead singer of the band. He like worked at the shop, worked at the shop, uh, and so I got him to sign my CD case. That's the guy that does Blues.

Chris Titley: He's more famous now for Blues Dad than the Custard, even though Custard were a tremendous band with such hits as Apartment and, uh, Music Is Crap and Girls Like That, etc. Um, but, uh, he's pretty more famous now. I think you go to the US and get on the talk show TV shows as opposed to where Custard ended up. But, um, now it's, uh, there you go, claim to fame. Uh, and the favorite beer?

Speaker C: Um, well, I was probably— what, you know, blew my mind in the beer world was when these like IPAs started coming out, which is very hoppy. I think India Pale Ales are coming out of New Zealand and Australia and the US. I think that everyone went way too hard at those, and everyone's probably just wanting to chill out a little bit more these days. So I'm probably more likely to go for a, for a pale ale. But as a, as a budding home brewer, I love to take like New Zealand hops and and Aussie wheat. I think it's like the best of both worlds. And so anything that, that, uh, is combining those things, uh, is pretty good for me.

Chris Titley: There you go, a little Australian— it should be— it'll be a ChatGPT creative name there for that sort of beer with Australian-New Zealand combo ingredients, etc. Um, excellent. Well, um, I look forward to the commercial success of your homebrew, firstly. And secondly, uh, thank you so much for telling the story, um, of Up and also the progress that you've you've made, uh, and the features that, that are within the app. And all the best to the, to the milestone of a million, as you mentioned, hopefully later on, uh, this year. Um, and looking forward to catching up soon.

Speaker C: Yeah, thanks, Chris. Great to be on. Listen to the Unfunded Podcast, brought to you by the Day One Network and hosted by me, tech writer Joan Westenberg. We're sharing the no-holds-barred untold stories from entrepreneurs who have decided to build a business on their terms. I'll be interviewing successful founders and operators on the grit and ingenuity it takes to build and scale independent startups without the support of traditional venture capital funding. Subscribe to the Unfunded Podcast now, wherever you get your podcasts.

{kind=link}